Justification Statement for 1513-0042 Non-significant Change

1513-0042 (F 5110.30) Non-significant Justification Statement.docx

Drawback on Distilled Spirits Exported

Justification Statement for 1513-0042 Non-significant Change

OMB: 1513-0042

August 11, 2025

Non-substantive Change Justification Statement for

OMB Control Number 1513–0042, Drawback on Distilled Spirits Exported

Under the Internal Revenue Code of 1986 (IRC) at 26 U.S.C. 5214(a)(4), distilled spirits may be withdrawn from a distilled spirits plant for export without payment of Federal alcohol excise tax, and under 26 U.S.C. 5062(b) persons who export tax-paid or determined distilled spirits may claim drawback (refund) of the excise tax paid on those spirits. Section 5062(b) also authorizes the Secretary of the Treasury to issue regulations governing such export drawback claims.

Among other things, the Alcohol and Tobacco Tax and Trade Bureau (TTB) administers the distilled spirits provisions of the IRC pursuant to section 1111(d) of the Homeland Security Act of 2002, as codified at 6 U.S.C. 531(d). The TTB regulations concerning distilled spirits export drawback are found in 27 CFR Part 28, Export of Alcohol. Under § 28.171, bottlers and packers of domestic distilled spirits on which alcohol excise tax has been paid or determined may claim drawback of that tax upon the export of such spirits to a foreign county or to U.S. Armed Forces stationed overseas, their ladening for use as supplies on certain vessels or aircraft, their transfer to a foreign-trade zone for export, or their transfer to a customs bonded warehouse for withdraw by certain foreign governments, officials, or organizations.

Specific to this information collection, approved under OMB control number 1513–0042, the TTB regulations 27 CFR 28.190, 28.192, 28.195b, and 28.199 require distilled spirits export drawback claimants to submit such claims using form TTB F 5110.30, Drawback on Distilled Spirits Exported. Currently on that form, in Item 12, drawback claimants may request payment of their drawback claim by check or as a credit to be taken on their alcohol excise tax return.

On March 25, 2025, the President issued an Executive Order, “Modernizing Payments To and From America’s Bank Account,” which was published in the Federal Register as E.O. 14247 on March 28, 2025, at 90 FR 14001. As a cost-saving and theft-prevention measure, the Executive Order requires, in general, that the Secretary of the Treasury cease issuing paper checks for all Federal disbursements, benefit payments, vendor payments, and tax refunds, and to make such payments via direct deposit or other electronic methods, effective September 30, 2025.

In response to E.O. 14247, TTB is revising form TTB F 5110.30 to eliminate the drawback claimant’s option to receive a paper check. Item 12 on the form will now allow the claimant to choose to receive their excise tax refund by direct deposit or as a credit to be taken on their alcohol excise tax return. In addition, if the claimant selects the direct deposit option, TTB has added Items 12a, 12b, and 12c to the form to allow the claimant to supply their direct deposit routing and bank account numbers, and to state if the account is a checking or savings account. TTB has also revised the instructions on the form to reflect the revision of Item 12.

TTB believes that these minor changes to TTB F 5110.30 made in response to E.O. 14247 do not affect this information collection’s per-respondent or total annual burden. The revision of Item 12 and the addition of Items 12a, 12b, and 12c merely require information that is already known by and immediately available to the respondent. These changes do not introduce new concepts and entail no burden other than that necessary to identify the respondent’s bank routing and account numbers to allow for direct deposit of an alcohol spirits excise tax refund, should the respondent select the direct deposit option. As such, TTB believes that these changes are non-substantive in nature, and we request OMB approval of the described changes to this information collection on that basis.

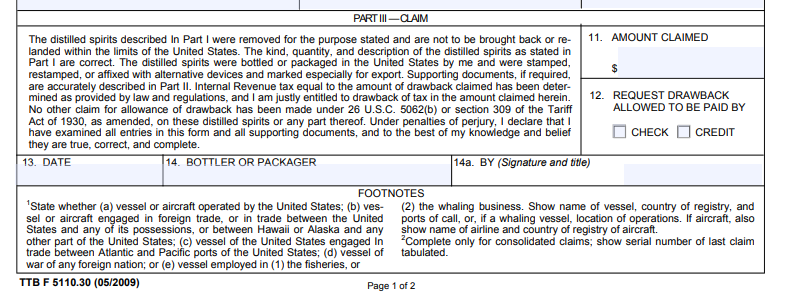

The figure below shows the previous version of Item 12 on TTB F 5110.30, Drawback on Distilled Spirits Exported, which allowed the respondent to select drawback payment of distilled spirits excise tax via a paper check or as a credit on their alcohol excise tax return:

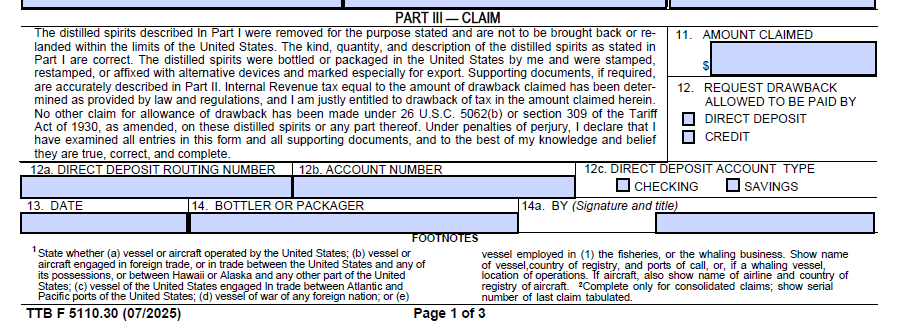

The figure below shows the new version of Item 12 on TTB F 5110.30, Drawback on Distilled Spirits Exported, allowing the respondent to select drawback payment of distilled spirits excise tax via direct deposit or as a credit on their alcohol excise tax return. If the respondent selects payment by direct deposit, they then provide their direct deposit routing number in Item 12a, their bank account number in Item 12b, and select the type of account—checking or savings—in Item 12c:

Instruction for Item 12 on the revised form:

[END]

| File Type | application/vnd.openxmlformats-officedocument.wordprocessingml.document |

| File Modified | 0000-00-00 |

| File Created | 2025-09-18 |

© 2026 OMB.report | Privacy Policy